Why Financial and ESG Reporting Are Converging

Financial reporting and sustainability reporting are increasingly converging. This was the focus of the presentation "Double Materiality Assessment (DMA) Using the European Sustainability Reporting Standards (ESRS) as an Example," delivered by ESG expert Oleksiy Yatsyuk at a webinar held by the Green Transition Office under the Ministry of Economy, Environment and Agriculture of Ukraine.

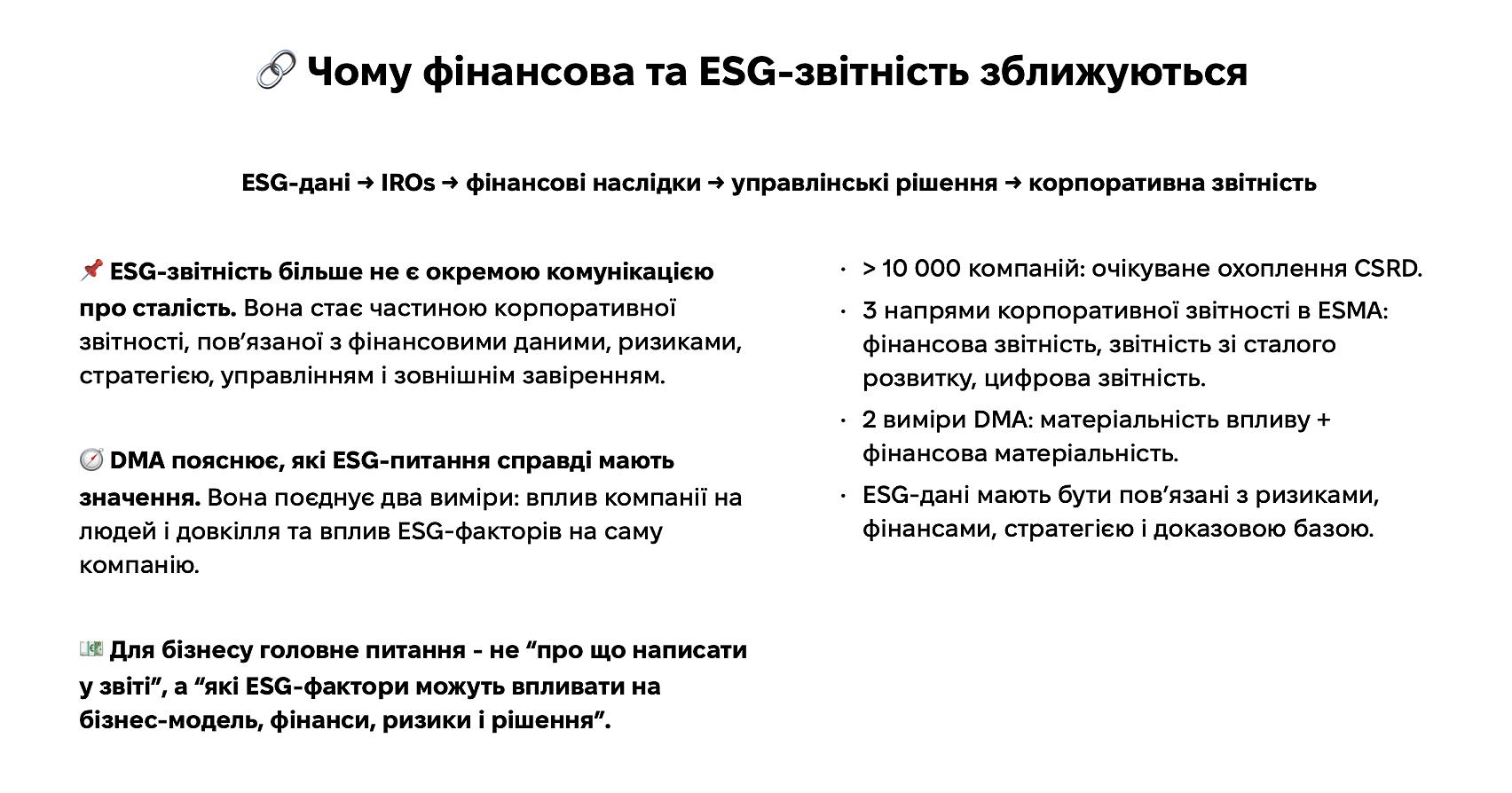

"ESG reporting is no longer a separate communication about sustainability. It is becoming part of corporate reporting, linked to financial data, risks, strategy, governance, and external assurance," said Oleksiy Yatsyuk.

According to him, DMA explains which ESG issues genuinely matter by combining two dimensions: a company's impact on people and the environment, and the impact of ESG factors on the company itself. The CSRD directive will cover more than 10,000 companies, and the European Securities and Markets Authority (ESMA) identifies three areas of corporate reporting: financial, sustainability, and digital.

Materiality itself sets the boundaries of reporting. A company does not disclose all ESG topics in equal detail, only those that are genuinely relevant to its operations, stakeholders, and report users. The focus is not on broad themes such as "climate" or "employees," but on specific impacts, risks, and opportunities, which DMA allows companies to assess, substantiate, and, where necessary, disclose.

When the discussion shifts from impact to financial consequences, an ESG factor is not in itself a financial risk. It becomes one only when it affects specific assets, costs, revenues, contracts, financing, or business strategy. Financial materiality is assessed based on the likelihood and scale of the effect, because it is not enough to simply identify a risk; companies need to understand how likely it is and what the financial consequences could be. In DMA practice, this assessment is typically conducted using a five-point scale, and the result must remain clear to financial and risk functions, since a financially material ESG risk is linked to budgets, investments, insurance, lending, asset valuation, or development scenarios.

According to EFRAG, it is at this intersection of financial and ESG reporting that the future of corporate reporting is being defined. That future does not lie in a mechanical merger of the financial report and the sustainability report, but in a stronger connection between them: consistent assumptions, data, and explanations. Report users should be able to trace a clear path from impacts, risks, and opportunities to strategy, capital investments, or other financial indicators. Materiality, in other words, has very practical significance for business: it works as a bridge between ESG, finance, and strategy.

The full study is available on the Green Transition Office website: Download (PDF)

The Green Transition Office is an independent advisory body under the Ministry of Economy of Ukraine that helps to implement reforms in the field of green transition, energy and climate policy of Ukraine. The Green Transition Office operates with the financial support of the UK International Development and is implemented by Dixi Group.

Published on